Credit Scores Explained

Credit Scores Explained

Why does your credit score go down after you pay off a loan? How does the scoring algorithm work? And the biggest lies about credit scores.

Hey everyone 👋 ,

Hope you're having a good week so far.

'Credit scores'...

A term that my 21 year old credit-card-spending self would squirm at the sound of.

But like it or not, credit scores are an integral part of our financial lives.

That dreaded three-digit number has a huge impact on whether we qualify for a mortgage, a car loan or an apartment lease. It can also determine how much we pay for home or car insurance.

But many people don't know how credit scores work. And there's a growing sense of frustration with the scoring algorithm.

So with that in mind, let's dive in.

Today I’ll cover:

Credit scores. A quick explanation📝

🧐 How does the credit score algorithm work

You’ve paid off your debt and your score has decreased. How?!

Five myths about credit scores

📹 60-second explainer on credit scores

Terminology worth knowing

Useful tools + resources

(Quickly) Explained…

Quite simply, a credit score is an easy and quick way for creditors (e.g. credit card companies, banks, loan agencies, etc.) to assess how big of a risk it would be to offer you credit.

If you have a history of living within your means and paying off your debts, then you’re a good customer for a company to give credit to because they have every reason to believe that you’ll pay it back.

But if you have a history of maxing out credit cards and not making car payments, then you are deemed a big risk that could cost the creditor even more money than the value of the loan offered.

Credit scores came about to ensure that lenders had a universal way to determine creditworthiness quickly and efficiently as more people needed credit and banks stopped being neighbourhood institutions that knew everyone's personal history.

🧐 How does the credit score algorithm work?

OK, so the best known and most widely used credit score is FICO, which rates consumers on a scale of 300 to 850.

And the higher your score, the better borrower you’re considered to be.

Your score is based on information from your credit reports with Experian, Equifax and TransUnion.

You can therefore have different scores depending on which credit file is accessed.

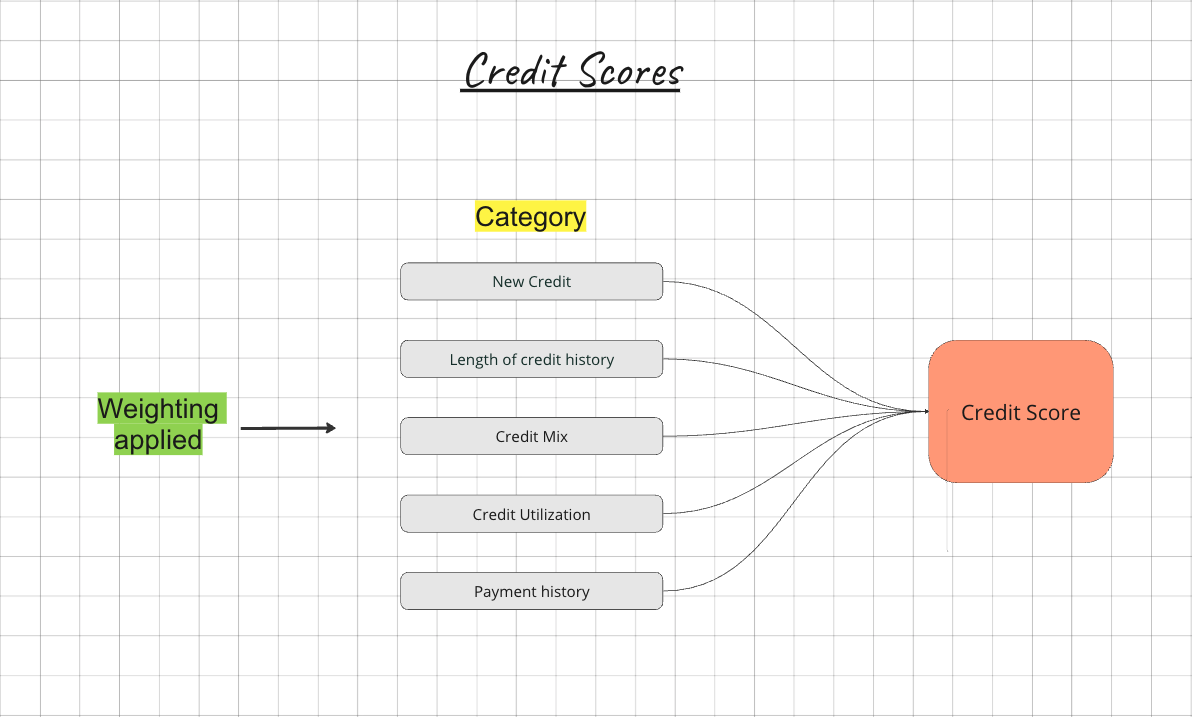

FICO scores are then calculated using data from your credit report, including payment history, amounts owed, new credit, length of credit history and mix of credit (such as mortgages and car loans).

Each category is weighted to reflect its importance in determining your score.

Payment history accounts for 35% of your score, followed by 30% for amounts owed or 'credit utilization', which is the amount of credit you're using compared to your total credit limit.

Your length of credit history is 15%. New credit accounts for 10%.

Your credit mix, which includes instalment loans (mortgages, auto loans, etc.) and revolving accounts (credit cards) also is weighted at 10%.

A mix of credit usage can demonstrate to lenders that you can obtain and manage different kinds of debt 🤹🏼♀️

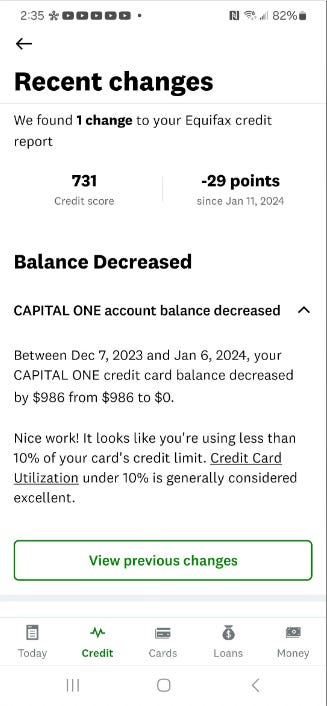

Scenario: You’ve paid off your debt and your score has decreased. How?!

But here’s why your score may drop after paying off a loan or a credit card.

Once you repay the loan or credit card, it’s no longer in the credit mix category.

FICO’s analysis of millions of consumer credit files has found that having a low installment-loan-balance-to-loan-amount ratio is simply a little less risky than having no active installment loans at all.

The elimination of data that demonstrates active, regular, on-time payments may mean some consumers see a temporary dip in their FICO scores.

However with time, you should see your score rebound as long as you continue to demonstrate positive credit behaviors such as on-time payments and a manageable level of overall debt.

Also, the FICO scoring system distinguishes between those who have never had an installment loan and those who have had years of this type of loan experience.

Credit Scores Myths 🗒️

There’s a bunch of misconceptions and myths around credit scores. Here’s a few to be wary of:

You only have one credit score

Not true! This misconception is often promoted by Credit Monitoring Services (CMS) or even credit card companies offering credit scores. They typically advertise providing "your credit score," suggesting there's only one definitive score, which is far from accurate.

In reality, individuals have numerous credit scores. Currently, there are around 40 different FICO score versions alone. Additionally, there's VantageScore, FICO's major competitor, offering two widely used models: VS3 and VS4. There’s also lesser-known models like TransUnion Rapid Default Model Version 1, utilized by institutions like US Bank in their lending decisions. Many lenders even develop their own proprietary scoring systems.

Among these, FICO 8 stands out as the most commonly used score for lending decisions today. You can access two out of three FICO 8 scores for free from myfico.com (Equifax FICO 8) and creditscore.com (Experian FICO 8).

Carrying a balance is necessary to improve your credit score

In reality, paying off your debt in full and on time can lead to an excellent credit score. Lenders prefer to see that you use credit responsibly, rather than maintaining a balance.

In fact The Consumer Financial Protection Bureau (CFPB) says that paying off your credit cards in full each month is actually the best way to improve your credit score and maintain excellent credit for the long haul.

Maintaining a credit utilization below 30 percent is essential

A significant portion of your credit score, about 30 percent, comprises the amounts owed or credit utilization, indicating how much credit you're using relative to your total credit limit.

Common advice suggests that individuals should aim for a credit card utilization rate of no more than 30 percent. For instance, if your credit card limit were $1,000, it's recommended to keep your balance at $300 or lower. This guideline applies to each individual credit card as well as the overall utilization across all your cards.

If you’re using a high percentage of your available credit, or you’re close to maxing out your credit cards, that can have a negative impact on your FICO score.

But the truth is that 30 percent ceiling isn’t a hard-and-fast rule. It’s a benchmark used to discourage consumers from overextending themselves.

If you’re aiming for a super high credit score, use a low percentage of your available credit. Low credit utilization can push you into an excellent credit range.

As of 2023, the average revolving credit card utilization was 6.5% percent for those with an 800-850 on the FICO scoring model.

Closing a credit card account is always a bad idea

While it's wise to consider your outstanding debt before closing a credit card account—doing so with balances can raise your overall credit utilization rate and potentially lower your credit score.

There are valid reasons to close an account. For instance, if the annual fee is too high or you're aiming to curb spending temptations.

If you've built a solid track record of responsible credit management, including timely bill payments and maintaining low credit card balances, closing an account may have minimal impact on your credit score. It's worth noting that an account in good standing, with a history of on-time payments, will remain on your credit report for up to 10 years after it's closed.

You are approved or denied credit because of your credit score

I come across this idea a lot. The thing is, it's not just about your credit score - it's your credit profile that really counts. Your credit profile has always been king in the world of credit, and that's not changing anytime soon.

People often say things like "your score is too low for that credit card," but the real issue is usually with your profile, not just your score. Think about the reasons lenders give for turning people down. Most of the time, it's stuff related to your profile, like recent late payments, too many inquiries, not enough income, high balances on your credit cards, having a collection on your record, opening too many accounts recently, or not having enough history with revolving credit.

You hardly ever hear them say "your score is too low."

There are plenty of cases where someone with, let's say, a score of 660 gets approved for a credit product, while someone with a score of 750 gets turned down for the same thing. If it was all about the score, you'd think the 750 score would win out. But it's not that simple; it's all about the profile and whether it fits the lender's criteria.

My main point here is that people often focus too much on that three-digit number and forget about the bigger picture - the overall profile. It's like missing the forest for the trees. If you concentrate on building a solid profile, higher scores will naturally come with time.

📹 How Your Credit Score Works…in 60 seconds

Terminology Worth Understanding

Credit Utilization Ratio: indicates how much credit you're using versus what's available.

Payment History ⏰: the most critical factor in your credit score. On-time payments help your score; missed payments harm it

Credit Mix: diversity in your credit accounts (e.g., credit cards, loans) can positively affect your score. It shows you can handle various types of credit

Hard Inquiries 🔍: occur when a lender checks your credit for a loan application. Too many can lower your score, signaling potential risk to lenders

Credit Age: the average age of your credit accounts. Older accounts contribute to a higher score by showing a longer history of credit use

New Credit: opening several new credit accounts in a short period can lower your score. It may indicate financial distress to lenders

Credit Report (Profile) 📜: a detailed record of your credit history from various sources. It’s crucial for calculating your score and identifying areas for improvement.

Tools + Resources 🧰

So let me start with my favourite, and that’s CreditRebels - essentially a very engaged community forum who’ve done extensive research into credit scores and have got so many tips on how to improve your score for free. This is the wikipedia of the credit score world in my humble opinion!

Credit Karma provides free credit scores and reports from TransUnion and Equifax that are updated weekly. And the best thing about this service is that you don't have to provide a credit card to register.

Finally, this is pretty cool - a credit score simulator

Thank you for sticking with me through this deep dive into credit scores and I hope you found it helpful 🙏 if you did I’d be super grateful if you could hit the ❤️ below -

Thank you!

Jason

DISCLAIMER: None of this is financial advice. Concepts of Finance newsletter is strictly for educational purposes.

Super helpful, thanks

This all makes sense, Jason. I'm based in Germany and have never borrowed money. I can imagine, though, that there's a similar system here that lets you and financial institutions assess how much you can borrow and under which conditions.